A new financial system – Financial Shenanigans #8

The brave new financial world.

Some weeks ago, I wrote about my belief in the future of decentralised systems. I see them being capable of fixing some of the inherent inequalities of our world, in a non-violent way. When it comes to centralised systems that require fixing, the financial system is perhaps the lowest hanging fruit there is.

To some extent, we have already seen plenty of disruption in financial services. Digital-only banks, like Revolut and N26, have become popular with the younger generation over the recent years. Personal trading is exceedingly done via apps like Robinhood, upending the traditional brokerage industry. And now the Covid-19 pandemic has accelerated the payments revolution towards contactless, benefiting companies like Square and PayPal. It's no surprise that both of them have introduced support for crypto purchases this year. Square went a step further, investing $50 million in Bitcoin, as a hedge against inflation and other macroeconomic risks.

Despite the above, I think we have barely scratched the surface. Over the next decade, a big chunk of financial services will transition to digital and decentralised alternatives. This transition will be facilitated by a wide range of crypto-native businesses, both decentralised and centralised ones. In all honesty, while centralisation debate is fundamental to most people in crypto, it's less relevant when comparing crypto-native businesses to traditional finance companies.

What most people are unaware of is that the movement to decentralise financial services, moving them onto a public blockchain has been underway for the last couple of years. In fact, plenty of traditional financial services have been replicated in crypto. These include but are not limited to lending and borrowing markets, exchanges, derivatives, asset management, insurance and market-making. It is true that, for the most part, these services are optimised for crypto assets. But there's plenty of work being done to tokenise a full range of real-world assets, from stocks to real estate. This would bring an unprecedented level of democratisation and fairness to financial services, removing century-old discriminatory policies and upending the industry long stuck in the past.

Here is a quote from Heath Tarbert, chairman of the U.S. Commodity Futures Trading Commission, to drive the point home.

The decentralised finance movement is "obviously revolutionary, and I think at the end of the day could lead to a massive disintermediation of the financial system and the traditional players."

This might sound overly abstract to some people so, as always, I'd like to give you an example. The area I'd like to focus on today is the lending and borrowing business. For decades, this has been the main business of financial institutions, their bread and butter. Banks would receive money from their customer as deposits and lend it out at a higher rate, thus generating profits. Central banks are another source of funding for the banks. Banks can borrow from their central bank at close to no cost while earning a significantly higher rate of return on a variety of lending products from credit cards to mortgages.

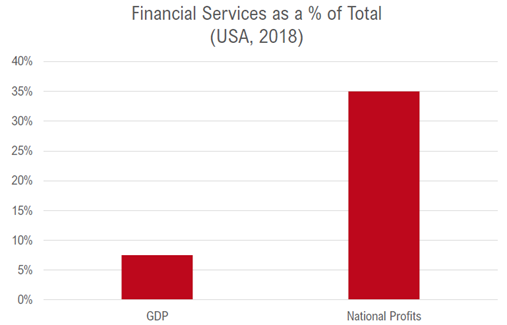

This is part of the reason why the financial services industry is the most profitable in the United States.

Needless to say that banks, like most other corporates, share very little of their profitability with customers instead choosing to reward executives and shareholders. Now, I probably don't need to go through the list of cool things the banks have done in the recent years, from the Wells Fargo scandal, Goldman's 1MBD shenanigans, numerous money laundering settlements, rigging of interest rates and so on.

Now, let's imagine that lending and borrowing activities are no longer conducted or intermediated by a bank. In fact, several crypto companies are in the lending and borrowing business, offering a much better product. There are decentralised protocols that facilitate this function, but also centralised companies. Each come with their own set of pros of cons.

Decentralised platforms facilitate lending & borrowing via smart contracts. Rates are set automatically, based on supply and demand for the asset. Smart contract code is open source and can be easily accessed and reviewed. Borrowing is available against collateral, with platforms often requiring substantial over-collateralisation and forced liquidations are triggered if the value of the collateral falls below a certain threshold. Pretty simple, right? No bank, no need for an intermediary, no discrimination. The primary benefit here, relative to centralised platforms, is that you maintain custody of your crypto assets. This means that you are the only one who can access them.

Centralised platforms, on the other hand, have custody of your digital assets. Another issue is that these guys also store your personal data, which you have to provide during the KYC verification process. This means that you are exposed to potential data breaches, and there's a probability, however small, of stolen funds. Good news is that the leading centralised work with trusted crypto custodians like BitGo and Gemini and carry a decent level of insurance cover.

Now, why would anyone use a centralised or a decentralised crypto platform for lending or borrowing? Simple, interest rates on offer. Let's move away from crypto for a moment and talk about stablecoins. They are still digital tokens but are pegged to a fiat currency, like USD or GBP. The first stablecoin was listed in 2015. Over the years, stablecoins have proven to hold a 1 to 1 peg to the USD, even in distressed market conditions. At the moment, investors can generate anywhere between 8 and 13% annual interest on stablecoins.

In the world where banks pay next to nothing, this is an attractive proposition. Users can also take out loans against crypto collateral, denominated in either fiat or a stablecoin. As you can imagine, interest rates on loans are also quite affordable due to the low risk, given the over-collateralisation.

With the current state of monetary and fiscal policy, it is unclear to me why anyone would hold their money in a bank. We have already seen the migration to digital-only offerings. In the future, we will also see the migration of funds from banks to both decentralised and centralised crypto lenders. As more real-world assets become tokenised, traditional financial functions like market-making, insurance and derivatives will also move into the new digital ecosystem. From a human perspective, we are moving to a more open and fair system. From an investment perspective, financial institutions will continue to see declining profitability for decades to come, making them uninvestable in the long-term.